5 Simple Techniques For How Home Mortgages Work

There are numerous options available for investing. These are generally contingent on your earnings, disposable cash, and long-term objectives. While saving for retirement, a second property financial investment, or otherwise can be a terrific goal, you might want to talk to a financial consultant about how to use your money most advantageously.

Property owners who desire to slash off dollars from their regular monthly home loan payment in addition to save money on interest, may consider a home mortgage recast. A mortgage recasting, or loan recast, is when a borrower makes a big, lump-sum payment towards the primary balance of their mortgage and the loan provider, in turn, reamortizes the loan.

Modifying cuts your regular monthly payments and the amount of interest you'll pay over the life of the loan. It does not, nevertheless, impact your interest rate or the regards to your loan. In this method, mortgage modifying deals 2 and potentially 3 appealing advantages for property owners with some additional money in their pocket to pay for the balance: Lower monthly payments.

If you have a low interest rate, that will remain the exact same. (On the other hand, if your rates of interest is high, recasting will not assist that.) In order to do a loan recast, customers need to make a large lump-sum payment towards the loan principal. Lenders typically need $5,000 or more to recast a mortgage.

There are normally costs related to recasting. The charges vary by loan provider; but they normally do not exceed a few hundred dollars. Recasting not only results in lower month-to-month payments but debtors will likewise pay less interest over the life of the loan. For example, if your 30-year mortgage carries a principal balance of $200,000 with a 5 percent rate of interest, you might pay $1,200 per month.

Not known Facts About What Does It Mean When People Say They Have Muliple Mortgages On A House

Obviously, the cash you sink into your home in the recast will not be available for investing or other functions. Remember, modifying does not decrease the term of your home mortgage, just how much you pay each month. Use our amortization schedule calculator to identify what your new monthly payments will be.

It's also not something that's generally advertised, however the majority of the huge banks offer it, including Chase, Bank of America and Wells Fargo. Plus, not all home loans get approved for modifying; some kinds of loans, wesley financial group dreams timeshare timeshare like FHA loans and VA loans, can't be modified. There's a huge distinction in between recasting a home loan and refinancing one, although both can help customers save money.

With recasting, you're keeping your existing loan, only changing the amortization. mortgages what will that house cost. You would not have the ability to get a lower interest rate with recasting, like you might with refinancing. On the other hand, if your rate of interest is already low then re-financing could have an unfavorable impact particularly if the present rates are greater.

The new loan would settle your existing loan, so you might wind up with a new mortgage as well as brand-new rates of interest. Individuals normally do this to get a lower rate of interest or to go from a variable-rate mortgage to a fixed-rate home loan. If you already have a fixed-rate home loan with a low rate of interest, then a refi wouldn't assist you.

Recasting has some appeal since it's relatively easy to do and it's a reasonably inexpensive way to decrease month-to-month payments if you have the money. Here are a couple of factors you might desire to consider recasting your existing mortgage: Lower your regular monthly payments by making one lump sum. Avoid needing to requalify for a new loan.

The 9-Second Trick For What Does Hud Have To With Reverse Mortgages?

The most significant monetary downside of recasting is that you're putting a large amount of money into equity. These are a couple of reasons you may desire to reconsider recasting: It does not shorten the length of your home loan. Your rate of interest remains the exact same, a downside if you have a greater rate of interest.

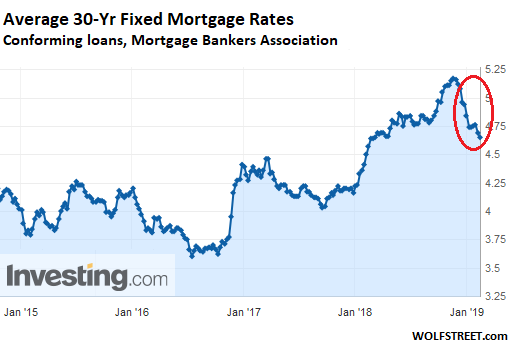

Lender charges a charge, normally no more than a few hundred dollars, to recast a loan. In the current climate, with fairly low home loan rates and a strong market, a loan recast may not make good sense for some.

Home mortgage recasting is one way to minimize your month-to-month home mortgage payments. It's less common than refinancing or modifying a loan, and it's hardly ever advertised, but it reduces home loan payments for those who can apply a swelling sum towards their loan's principal. When you modify your mortgage, you pay your lending institution a large sum toward your principal, and your loan is then reamortized simply put, recalculated based upon your brand-new, lower balance.

It's a transfer to make if you wish to minimize your interest cost without reducing your loan term, states Eric Gotsch, a sales manager for Wells Fargo House Home Mortgage (mortgages what will that house cost). The most common factor for recasting is if you have actually purchased a home however not yet offered your previous one, states Jim Hettinger, executive vice president of operations at Guaranteed Rate, an online mortgage lending institution.

Modifying is also perfect wesley financial group fees for individuals who get a big amount of money and want to lower their home mortgage costs, Gotsch states. This typically occurs when somebody gets an inheritance, a financial investment distribution or a big bonus, or has a nontraditional earnings stream, he says. In the majority of cases, you'll need at least $5,000 to modify your home mortgage.

The Basic Principles Of Which Congress Was Responsible For Deregulating Bank Mortgages

When you refinance, you secure a new loan, with various terms, to replace the old one. You could get a lower interest rate or switch from an adjustable to a fixed rate or from 15 years to thirty years, for example. The benefit of a mortgage recast is basic: It reduces your regular monthly payments, making your housing expenses more inexpensive.

You won't require a credit check or an appraisal to recast, making it an easier option than refinancing. There's a great chance that it will be less expensive than refinancing, too, considering that you will not face the typical range of closing costs. However, you might need a history of on-time payments to modify.

Loans bought by Fannie Mae and Freddie Mac can be modified, he states, but Federal Housing Administration and Veterans Affairs loans can't. Additionally, jumbo or nonconforming home mortgages might be eligible for recasting just on a case-by-case basis, Hettinger states. Some lending institutions charge a cost for the service, usually a couple of hundred dollars, so inquire about the cost.

" There are likewise varying policies relating to just how much a customer will need to put down to recast the loan," Hettinger states. "Make certain you have your loan officer contact the servicer prior to entering into a closing presuming you can recast a few months down the line." Lenders who offer recasting generally do not promote it.

We will never ever reveal or sell your email address or any of your information from this website. We do extremely welcome posts and neighborhood interaction, and signing up is just part of the posting system. Financial Samurai exists to believed provoke and find out from the neighborhood. Your decisions are yours alone and we remain in no method accountable for your actions.

Opmerking

Welkom bij

Beter HBO

© 2024 Gemaakt door Beter HBO.

Verzorgd door

![]()

Je moet lid zijn van Beter HBO om reacties te kunnen toevoegen!

Wordt lid van Beter HBO